“Did you see that Geico commercial? They are giving money back because of Coronavirus!! I love that company.”

my wife. The worlds only consumer who loves an insurance company

I don’t use Geico insurance anymore, even though I do love their advertising and my wife has an unnaturally strong brand preference for the Gecko. She actually loves the company. They sell insurance. Not exactly a product normal people have an affinity for. But if you have a heartbeat, you know the brands – the advertising spend total for all insurers is $6.7 Billion – (the top 10 are 82% of total) – the total TV advertising revenue is $62.23 Billion. Sure, not all $6.7 B is spent on TV but its seems like it and that will earn you some brand recognition. Why don’t I use Geico? I have a close friend who runs an Allstate agency and as he says to me all the time….”Insurance isn’t funny. It’s a calling, not a job.” Its not the most compelling argument but he’s a good friend, Allstate has fine coverage and I am a lazy consumer* (*aka sticky customer).

(quick aside on Ad spending: Did you know Expedia spends > $5Bill on advertising? Chairman Barry Diller says they are dropping ad spending 80% from $5B to $1B! that is definition of pro-cyclical )

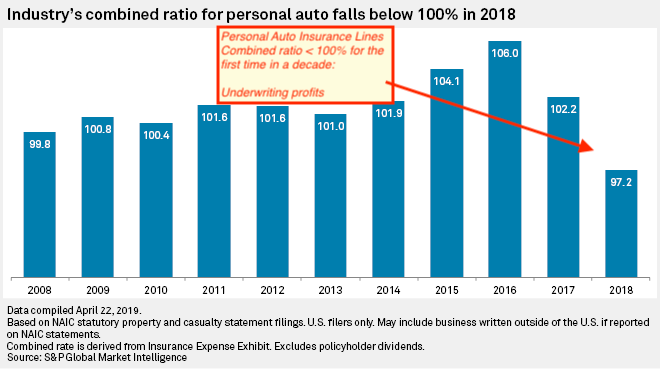

Insurance companies are giving $$ back because no-one is driving. And it’s not just Geico. All the insurance carriers (including AllState) are offering rebates but its not out of kindness. Claims = accident frequency X severity. So they are proactively lowering their premiums. I would bet their claims are dropping way more then their premiums. I’m sure they will lose some premium revenue as some policies are cancelled, but overall the revenue stream is highly defensive and getting more profitable with less claims. And overall they are starting in a healthy profit position with a combined ratio for the auto insurance industry below 100 for the first time in a decade ~ 97.2. (Below 100 = the industry is making an underwriting profit)

COTW #1 (Chart of the Week)

COTW #2 and #3 – Gasoline Demand at All-Time Low, Supply at All-Time High

Subscription Payment Plans are not Utility Models

We don’t usually get variable pricing based on how much we drive. While I appreciate the break on my bill, I still get the autopay notification every month that I’m paying that premium. Like everyone else – I am not using any gasoline or driving anywhere. Yet I am still paying for insurance. It’s just on a convenient payment plan.

Infrastructure as a Service can be Utility model or a Payment Plan (and its at an inflection point)

I have spent some quality quarantine-ing time (QQT) getting deeper into Data Economics in general and the current state of the market specifically in ‘as-a-Service offerings’, cloud costs and utility models. When you are building and operating an enterprise you are using a wide range of technology stacks and financing it via combination of utility model (usage), subscription and lease payment plans, capex and depreciation schedules, etc. And while not difficult to understand topics, it does require some work to get grounded in the fundamentals if it’s not your primary domain.

According to IDC – we are about to see a huge acceleration of IaaS spending (Infrastructure as a Service). I absolutely agree with this call and I am seeing this everyday in my business. It is the perfect time to get grounded in the fundamental building blocks of the offerings. Buying a car, leasing a car and taking an Uber all provide transportation but very different experiences. And I don’t pay for insurance, gas or car washes for my Uber driver.

The Corona-Recession is going to Challenge Recurring Revenue Forecasts

The inevitable Corona-recession is going to test the recurring revenue consensus view. I highly recommend this read by Gavin Baker of Atreides Managment.

Software contracts, first-lien debt and the reality that no revenue is truly recurring. Robert Smith, CEO and founder of Vista Equity Partners famously said: “Software contracts are better than first-lien debt. You realize a company will not pay the interest payment on their first lien until after they pay their software maintenance or subscription fee. We get paid our money first. Who has the better credit? He can’t run his business without our software.”

While he is talking specifically about Software – it is thought provoking and just as applicable to IaaS or cloud in my view. My main takeaway – – its not the payment model or go-to-market model that will provide defensible revenue – its the actual hard ROI of the software underneath the offering.

While its not likely I will switch my auto insurance – I probably should. Its best practice to switch your provider every 2 years. 15 minutes could save you more than 15% in this market.